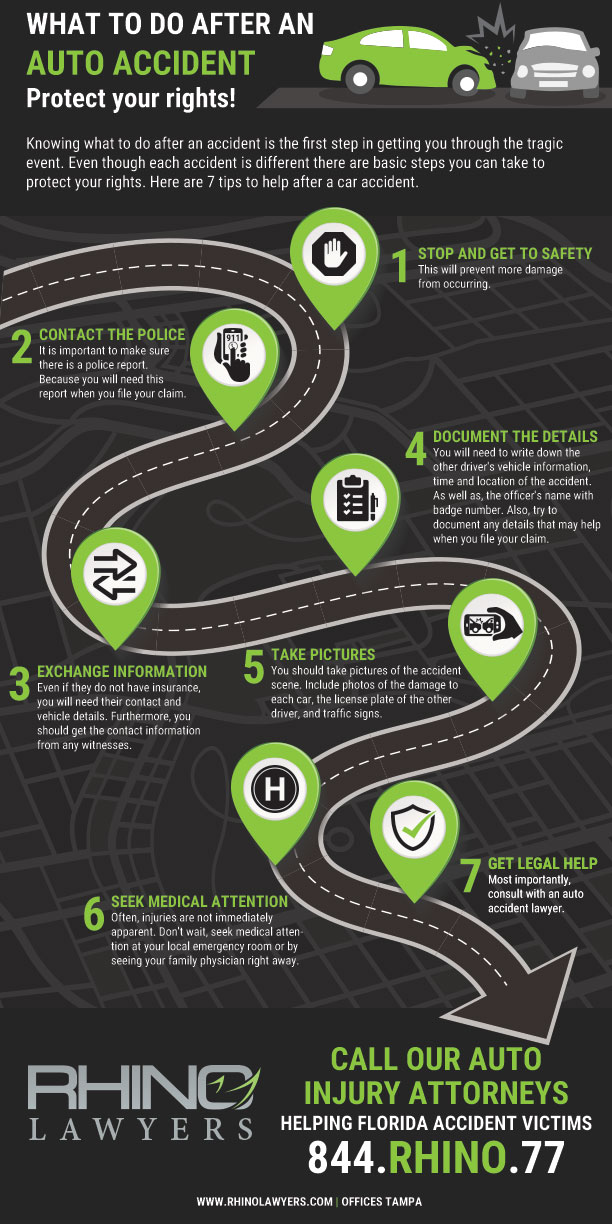

One of the most common traffic accidents is due to driver distraction. In 2018 distracted driving was responsible for the deaths of 2,000 people in the United States. This puts you at high risk of a collision with a distracted driver, even if you are a cautious driver. Do you know that under Florida’s no-fault law you only have 14 days to preserve your insurance benefits? If you receive a ticket, that does not remove your ability to receive no-fault compensation. Even if you are not feeling any impact on your health at this time, preserve your ability to later file a claim by contacting a personal injury lawyer today.

There are only 14 states that have no-fault insurance, and Florida is one. Read on for all the “must-know” information about no-fault auto insurance law.

What Does No-Fault Mean?

In the majority of states, the driver found at fault in an accident is responsible for covering all the expenses the other driver incurs as a result of that collision. Florida is one of a few states with a no-fault auto insurance law. This means each person uses their own insurance coverage to cover their damages.

The advantage to no-fault insurance is that regardless of who is at fault in a car accident, liability for expenses falls on each individual’s personal auto insurance. This allows claims to move quickly and those suffering from injuries obtain coverage for their expenses faster.

No-Fault Insurance Coverage

Every automobile in Florida must carry Personal Injury Protection (PIP) insurance. This provides coverage to you and others in your household who are in an automobile accident, your vehicle passengers, and persons who are hit by your automobile and were not in another vehicle (i.e. pedestrians, those on a bicycle, etc.) Entitlement to this insurance coverage is guaranteed regardless of which driver is at fault.

There are minimum amounts of coverage you need to purchase which covers bodily injury and property damages. This is written on your policy as 10/20/10. What this means is:

- $10,000 for bodily injuries to one person

- $20,000 total body injuries in any number of persons in one accident

- $10,000 for property damage

The minimum coverage amounts are very low in comparison to the average costs incurred for medical treatment, so it is always advisable to increase the amount of coverage you have.

What many don’t realize is that Florida Statute §627.730 not only requires owners to have insurance, but it also requires non-resident owners who have their own automobile in Florida for more than 90 days to have no-fault insurance. This means that snowbirds who do not reside in a no-fault state but spend more than 90 days in Florida over the winter months must purchase no-fault insurance.

You should also be aware that motorcycles do not have a PIP coverage requirement. That is because this type of vehicle does not fall under the “motor vehicle” definition under the law. If your automobile collides with a motorcyclist, the rider will be treated as if you hit a pedestrian.

What PIP Pays

Personal Injury Protection does not cover medical expenses in full. The required benefits are set forth in Florida Statute §627.736 and cover 80% of reasonable medical expenses including surgery, x-rays, dental, and rehabilitation services. To receive coverage medical care must be initiated within 14 days of the accident.

It will also pay a death benefit of $5,000, a 60% lost wage benefit, and 100% of replacement services. Replacement services are those things you must hire done because your injuries prevent you from performing them yourself. This includes things such as mowing the lawn, doing laundry, cleaning your house, etc.

Insurance Deductible

The deductibles you have on your policy must be paid before the insurance coverage kicks in. That means if you have a $1,000 deductible and $4,000 in medical bills, you must pay the $1,000 deductible, after which 80% or $3,200 of your medical bills will be paid by the insurance.

To make sure you have better coverage in the event of a catastrophic accident, talk to your insurance provider about increasing your coverage amounts under no-fault insurance. Medical payment riders will provide coverage for additional medical bills after your PIP insurance coverage reaches the maximum.

Does Everyone Need to Buy No-Fault Insurance?

In Florida, everyone who registers a car must have no-fault insurance coverage. If you do not own a vehicle then you do not have an obligation to purchase insurance. Although if someone else in your household owns an automobile, you may have PIP coverage through their insurance.

If no one in your household owns a vehicle and you suffer injuries, the other driver’s personal injury protection (PIP) may help cover your medical expenses.

Florida No-Fault Law Impact on Lawsuits

If you suffer serious, permanent injuries in a car accident Florida’s no-fault insurance law may not apply. Injuries of this nature fall under Florida Statute §627.737. This law makes every owner and operator of motor vehicles legally responsible for losses incurred as a result of their negligent motor vehicle operation.

Your personal injury attorney will evaluate your injuries to see if they meet the qualifications for tort law or no-fault coverage. You may need to file a lawsuit regarding no-fault coverage if your insurance company does not cooperate with paying your claim. The lawsuit may be against your own or the other driver’s insurance company for not providing appropriate coverage.

In this type of lawsuit, the claim deals with the insurance company failing to pay your PIP benefits. This means the insurance company is acting in bad faith. There is no need to prove which driver is at fault.

A Personal Injury Attorney Can Help

Navigating Florida’s no-fault law can be confusing. You need knowledge of Florida law, insurance law, accident law. You must also have the ability to understand medical records and terminology.

If you have been injured in an accident we can help you receive the compensation you deserve under Florida no-fault law. We are available 24/7 and you have the option of contacting us by phone or text message at (844) 932-0568. You may also request a free instant case valuation using our online form, and for your safety, we offer video consultations.

When filing a personal injury claim, we only receive a payment if we win your case. Consultations are free and with no up-front attorney fees, you have nothing to lose. Contact us today for a free evaluation of your rights under Florida no-fault law.

CONTACT A TAMPA AUTO ACCIDENT ATTORNEY

In short, after a car accident, you may not know your rights. Above all, don’t struggle through the process alone. Actually, our personal injury team is here to help you with any legal needs you might have regarding your accident.

Lastly, let RHINO Lawyers answer your questions and review the facts of your case with a Free Consultation. So, get started by completing the “Free Instant Case Evaluation” or by calling us any time, day or night, at 844.329.3491.