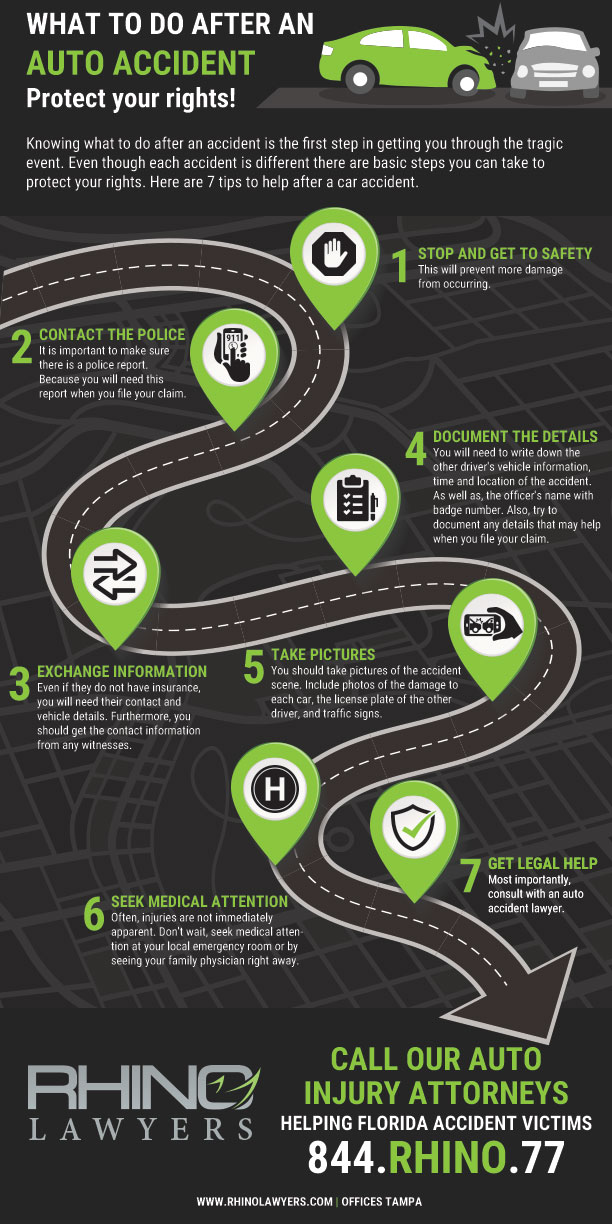

Driving in Florida can be a constant struggle. With the traffic, distractions, and amount of uninsured motorists on the roadways, car accidents happen all the time. However, even though a driver may be “at fault” in the accident, that does not mean that they have insurance to cover your injuries.

Why is UM important?

Florida is a “no-fault” state and requires drivers to carry personal injury protection (PIP) insurance. However, bodily injury insurance is not necessary. This means the insurance company may take on the liability. Also, that the person who injured you may be able to protect themselves, but not have any money to cover your injuries. Due to this problem, many people in Florida carry uninsured/underinsured motorist coverage (UM).

Florida statute 627.727 allows injured drivers to carry their own insurance to protect themselves from drivers who do not have the insurance to cover the injured drivers’ damages. To mirror the automobile liability coverage on the policy Florida created uninsured/underinsured motorist coverage. Florida’s public policy is that every insured driver can recover damages. So the damages afforded would be the same as an at-fault driver with a bodily injury liability policy. Here is an example:

Mary is driving on a roadway and decides to adjust the radio. Traffic ahead stopped and Jim has stopped at the red light. Distracted Mary rear-ends Jim’s car damaging both cars. Injured in the accident Jim incurs medical bills. Mary has insurance, but her insurance covers property damage and her personal injury protection, not the bodily injury of another. Jim’s treatment costs money, but he cannot get reimbursed from Mary’s insurance coverage. However, Jim’s own insurance has UM coverage to protect him. This means that Jim use his own insurance to get reimbursed for the medical bills and pain and suffering he underwent through the length of his treatment after the accident.

What does it do for me?

By having uninsured/underinsured (UM) coverage, you help to protect yourself from drivers on the road who are not carrying insurance. Insurance companies must have a written rejection that someone does not want UM coverage. Otherwise, they may have to pay out what the bodily injury coverage would be. This means that if your insurance policy has bodily injury coverage, you have the ability to have UM coverage up until that amount as well. Having the UM coverage allows you to recover future medical expenses, lost wages, and non-economic damages like a permanent disability of pain and suffering. Your personal injury protection coverage and health insurance will pay for the present bills. But during the course of treatment, the future medical expenses can get paid through any coverage, which includes UM coverage.

What should I do?

If you have additional questions about an accident you were in and injuries you suffered as a result, contact RHINO Lawyers. Our personal injury team will explore all options of the accident, including all insurance areas to make sure you are getting the help you deserve. Give us a call at 844-RHINO-77 for a free consultation. Take Charge of your Rights.